|

|

The "Liebl Method" is a set of procedures which allows us to solve capitalization

plans and amortization systems problems derived from uniform series and

arithmetic progression series, making use of a single generic formula.

Therefore it deals with the French System of Amortization, the American

System, the Canadian Mortgage, the German System, the Series in Crescent

and Decreasing Gradients, the Compound System of Amortization with Real

Crescent Installments, the Constant Amortization System and the Compound

System of Amortization, as well as the capitalization of the respective

series.

It can be operated by calculators that have the SOLVER function, reaching its full potential with calculators that deals with algebraic object - as the ones from the family of the Hewlett Packard 48 - and with the EXCEL electronic spread sheet from Microsoft.

PV - PRESENT VALUE

Present value, also known as actual value, capital, principal, loan

value or value of the financing.

i - INTEREST RATE

Unitary interest rate, compatible with the periodicity to what the

"n" variable refers itself. For practical effects, the variable "i" can

be substituted in the formula by the expression " I% / 100 ", where " I%

" corresponds to the percentile rate of interest.

m - PAYMENT MODE

Mode through which the first payment of the series starts: anticipated,

postponed or deferred. The default is zero and corresponds to the

postponed. The anticipated method holds the value -1 (one negative), while

the deferred depends on the delay term, and is expressed in compatible

periodicity to which refers the variable "n".

n - NUMBER OF PAYMENTS

Number of payments, also known as quantity of installments, number

of compounding periods, time or term.

PMT - PAYMENT VALUE

Value of the payment, also known as value of the installment.

G - GRADIENT VALUE

Value of gradient, also known as increase or decrease rate, or positive

or negative rate, related to the series in increasing or decreasing arithmetic

progression.

FV - FUTURE VALUE

Future value.

The variables assume positive or negative values, depending, basically, on the flow (debits and credits) of the money in the period, on the kind of capitalization or system of amortization which is being considered, and on the payment mode (anticipated, postponed or deferred) to which the problem refers itself.

Next, will be presented the BASIC PARAMETERS TO THE DATA ENTRY:

1 FRENCH SYSTEM OF AMORTIZATION

|

|

|

|

|

|

|

|

|

| Postponed mode |

|

|

|

|

|

|

|

| Anticipated mode |

|

|

|

|

|

|

|

| Deferred mode |

|

|

|

|

|

|

|

2 CAPITALIZATION OF UNIFORM SERIES

|

|

|

|

|

|

|

|

|

| Focus date = N |

|

|

|

|

|

|

|

3 AMERICAN SYSTEM

|

|

|

|

|

|

|

|

|

| With interest paid during the waiting period |

|

|

|

|

|

|

|

| With interest capitalized during the waiting period |

|

|

|

|

|

|

|

| Formation of the "Sinking Fund" |

|

|

|

|

|

|

|

4 CANADIAN MORTGAGE

|

|

|

|

|

|

|

|

|

| Postponed mode |

|

|

|

|

|

|

|

Formula to calculate the I%:

5 GERMAN SYSTEM

|

|

|

|

|

|

|

|

|

| Interest calculated and collected in advance |

|

|

|

|

|

|

|

6 SERIE IN CRESCENT GRADIENT

|

|

|

|

|

|

|

|

|

| 1st.PMT=G

Postponed mode |

|

|

|

|

|

|

|

| 1st.PMT=G

Anticipated mode |

|

|

|

|

|

|

|

| 1st.PMT=G

Deferred mode |

|

|

|

|

|

|

|

| 1st.PMT#G

Posponed mode |

|

|

|

|

|

|

|

7 CAPITALIZATION OF SERIES IN CRESCENT GRADIENT

|

|

|

|

|

|

|

|

|

| 1st.PMT=G |

|

|

|

|

|

|

|

| 1st.PMT#G |

|

|

|

|

|

|

|

8 COMPOUND SYSTEM OF AMORTIZATION WITH REAL

CRESCENT INSTALLMENTS

|

|

|

|

|

|

|

|

|

| 1st.STAGE:

PMT calculation |

|

|

|

|

|

|

|

| 2nd.STAGE: Calculation of the balance in the date of the 23rd PMT with reducer |

|

|

|

|

|

|

|

| 3rd.STAGE: Calculation of the growth ratio |

|

|

|

|

|

|

|

9 SERIE IN DECREASING GRADIENT

|

|

|

|

|

|

|

|

|

| Final

PMT = G Postponed mode |

|

|

|

|

|

|

|

| Final

PMT = G Anticipated mode |

|

|

|

|

|

|

|

| Final

PMT = G Deferred mode |

|

|

|

|

|

|

|

| Final

PMT # G Posponed mode |

|

|

|

|

|

|

|

10 CAPITALIZATION OF SERIES IN DECREASING

GRADIENT

|

|

|

|

|

|

|

|

|

| Final

PMT = G |

|

|

|

|

|

|

|

| Final

PMT # G |

|

|

|

|

|

|

|

11 CONSTANT AMORTIZATION SYSTEM

|

|

|

|

|

|

|

|

|

| Postponed mode |

|

|

|

|

|

|

|

12 COMPOUND SYSTEM OF AMORTIZATION

|

|

|

|

|

|

|

|

|

| Postponed mode |

|

|

|

|

|

|

|

The "Liebl Method" was tested in two types of Hewlett Packard calculators, a financial and a scientific one, through its SOLVER function, and, also, in the EXCEL electronic spread sheet from Microsoft.

It was chosen to substitute, in the generic formula, the variable "i" for the correspondent to the percentile rate of interest, ( I% / 100 ), due to the practicability that it offers.

There must be observed the insertion of the necessary parenthesis, as well as the correct transcription of the symbols of operations (power of a number, multiplication, division, addition and subtraction) in order not to occur incorrect calculations in the conversion of the formula for SOLVER functions.

Example:

TRANSCRIBED FORMULA TO THE HP 48 SX CALCULATOR SOLVER FUNCTION:

| PV*(1+I%/100)^(M+N)+((PMT+G/(I%/100))*((1+I%/100)^N-1)-G*N)/(I%/100)+FV=0 |

EXAMPLE OF USE IN THE EXCEL ELECTRONIC SPREAD SHEET FROM MICROSOFT:

DEFINITION OF THE CELLS:

|

|

|

|

|

|

|

Present value |

|

|

|

Interest rate |

|

|

|

Payment mode |

|

|

|

Number of payments |

|

|

|

Payment value |

|

|

|

Gradient value |

|

|

|

Future value |

|

|

|

Present value of extra payments |

|

|

|

Equalizer |

METHOD OF OPERATION:

1. All variables are filled with the data of the problem, except the one which solution is being searched;

2. Select the button corresponding the cell of the variable which solution is being searched;

3. The solution for the problem will be presented in this corresponding cell.

Next, will be presented examples of solution of problems using the "LIEBL METHOD":

1.1 FRENCH SYSTEM

OF AMORTIZATION

Postponed mode

A $ 10,000.00 loan, acquired at the rate of 10% per month, will be paid in 4 monthly installments through the French System of Amortization, with the first installment to be paid one month after the business transaction. What will be the installment value?

|

|

|

|

|

|

-10,000.00

|

|

|

|

10.000000

|

|

|

|

0.00

|

|

|

|

4.00

|

|

|

|

TO SOLVE

|

3,154.71

|

|

|

0.00

|

|

|

|

0.00

|

|

Answer: The installment value will be $ 3,154.71.

| EVOLUTION SPREAD SHEET | ||||

| N | PAYMENT | INTEREST | PRINCIPAL | BALANCE |

| 0 | 10,000.00 | |||

| 1 | 3,154.71 | 1,000.00 | 2,154.71 | 7,845.29 |

| 2 | 3,154.71 | 784.53 | 2,370.18 | 5,475.11 |

| 3 | 3,154.71 | 547.51 | 2,607.20 | 2,867.92 |

| 4 | 3,154.71 | 286.79 | 2,867.92 | 0.00 |

| TOTAL | 12,618.83 | 2,618.83 | 10,000.00 | |

1.2 FRENCH SYSTEM

OF AMORTIZATION

Anticipated mode

A domestic device that costs $ 1,000.00 can be acquired with a rebate of 20% for payment in cash or in 4 monthly installments without accretion. The first installment must be paid at the purchase. What is the monthly interest rate inserted in the operation?

Note: The PV is the value of purchase deduced the rebate offered for

the payment in cash.

|

|

|

|

|

|

-800.00

|

|

|

|

TO SOLVE

|

17.2687

|

|

|

-1.00

|

|

|

|

4.00

|

|

|

|

250.00

|

|

|

|

0.00

|

|

|

|

0.00

|

|

| EVOLUTION SPREAD SHEET | ||||

| N | PAYMENT | INTEREST | PRINCIPAL | BALANCE |

| 0 | 800.00 | |||

| 0 | 250.00 | 0.00 | 250.00 | 550.00 |

| 1 | 250.00 | 94.98 | 155.02 | 394.98 |

| 2 | 250.00 | 68.21 | 181.79 | 213.19 |

| 3 | 250.00 | 36.81 | 213.19 | 0.00 |

| TOTAL | 1,000.00 | 200.00 | 800.00 | |

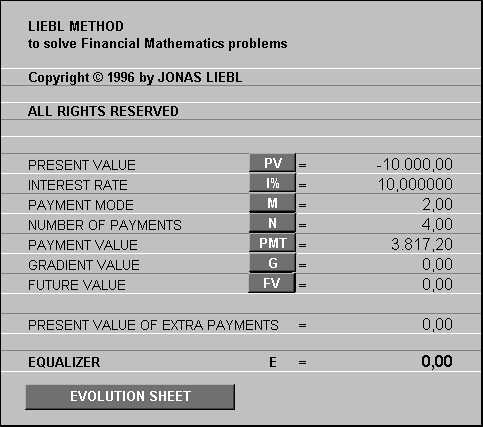

1.3 FRENCH SYSTEM

OF AMORTIZATION

Deferred mode

A $ 10,000.00 loan, acquired at the rate of 10% per month, will be paid

in 4 monthly installments through the French System of Amortization. The

first installment is to be paid three months after the business transaction.

What will be the installment value?

|

|

|

|

|

|

-10,000.00

|

|

|

|

10.000000

|

|

|

|

2.00

|

|

|

|

4.00

|

|

|

|

TO SOLVE

|

3,817,20

|

|

|

0.00

|

|

|

|

0.00

|

|

Answer: The installment value will be $ 3,817.20.

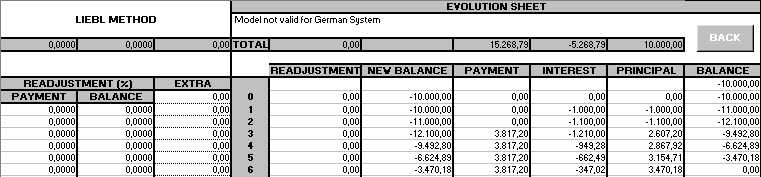

| EVOLUTION SPREAD SHEET | ||||

| N | PAYMENT | INTEREST | PRINCIPAL | BALANCE |

| 0 | 10,000.00 | |||

| 1 | 0.00 | 1,000.00 | -1,000.00 | 11,000.00 |

| 2 | 0.00 | 1,100.00 | -1,100.00 | 12,100.00 |

| 3 | 3,817.20 | 1,210.00 | 2,607.20 | 9,492.80 |

| 4 | 3,817.20 | 949.28 | 2,867.92 | 6,624.89 |

| 5 | 3,817.20 | 662.49 | 3,154.71 | 3,470.18 |

| 6 | 3,817.20 | 347.,02 | 3,470.18 | 0.00 |

| TOTAL | 15,268.79 | 5,268.79 | 10,000.00 | |

2.1 CAPITALIZATION OF UNIFORM SERIES

How much would a person collect if made 5 monthly deposits of $ 1,000.00 in a financial institution which pays 5% per month?

Note: In the capitalization of series of payments, uniform or gradient,

the focus date will be always the date of the last payment, not existing,

however, any difference among the postponed, anticipated or deferred mode.

|

|

|

|

|

|

0.00

|

|

|

|

5.000000

|

|

|

|

0.00

|

|

|

|

5.00

|

|

|

|

1,000.00

|

|

|

|

0.00

|

|

|

|

TO SOLVE

|

-5,525.63

|

Answer: The person would collect $ 5,525.63.

| EVOLUTION SPREAD SHEET | ||||

| N | DEPOSIT | INTEREST | CAPITALIZATION | BALANCE |

| 1 | 1,000.00 | 0.00 | 1,000.00 | 1,000.00 |

| 2 | 1,000.00 | 50.00 | 1,050.00 | 2,050.00 |

| 3 | 1,000.00 | 102.50 | 1,102.50 | 3,152.50 |

| 4 | 1,000.00 | 157.63 | 1,157.63 | 4,310.13 |

| 5 | 1,000.00 | 215.51 | 1,215.51 | 5,525.63 |

| TOTAL | 5,000.00 | 525.63 | 5,525.63 | |

3.1 AMERICAN SYSTEM

With interest paid during the waiting period

A financial institution lends $ 50,000.00 through the American System.

This quantity will be amortized after 5 years. What will be the value of

the payments, knowing that the interest are annually paid at a rate

of 12% per annum?

|

|

|

|

|

|

-50,000.00

|

|

|

|

12.000000

|

|

|

|

0.00

|

|

|

|

5.00

|

|

|

|

TO SOLVE

|

6,000.00

|

|

|

0.00

|

|

|

|

50,000.00

|

|

Answer: The value of the annual payment is $ 6,000.00.

| EVOLUTION SPREAD SHEET | ||||

| N | PAYMENT | INTEREST | PRINCIPAL | BALANCE |

| 0 | 50,000.00 | |||

| 1 | 6,000.00 | 6,000.00 | 0.00 | 50,000.00 |

| 2 | 6,000.00 | 6,000.00 | 0.00 | 50,000.00 |

| 3 | 6,000.00 | 6,000.00 | 0.00 | 50,000.00 |

| 4 | 6,000.00 | 6,000.00 | 0.00 | 50,000.00 |

| 5 | 56,000.00 | 6,000.00 | 50,000.00 | 0.00 |

| TOTAL | 80,000.00 | 30,000.00 | 50,000.00 | |

3.2 AMERICAN SYSTEM

With interest paid during the waiting period

Formation of the "Sinking Fund"

In order to prevent a big outlay on the payment date, the debtor, from

the previous example, constitutes an amortization fund at a financial institution,

which pays 10% per annum. What will be the value of the annual deposits?

|

|

|

|

|

|

0.00

|

|

|

|

10.000000

|

|

|

|

0.00

|

|

|

|

5.00

|

|

|

|

TO SOLVE

|

8,189.87

|

|

|

0.00

|

|

|

|

-50,000.00

|

|

Answer: The value of the annual deposits will be $ 8,189.87.

| EVOLUTION SPREAD SHEET | ||||

| N | DEPOSIT | INTEREST | CAPITALIZATION | BALANCE |

| 1 | 8,189.87 | 0.00 | 8,189.87 | 8,189.87 |

| 2 | 8,189.87 | 818.99 | 9,008.86 | 17,198.74 |

| 3 | 8,189.87 | 1,719.87 | 9,909.75 | 27,108.48 |

| 4 | 8,189.87 | 2,710.85 | 10,900.72 | 38,009.21 |

| 5 | 8,189.87 | 3,800.92 | 11,990.79 | 50,000.00 |

| TOTAL | 40,949.37 | 9,050.63 | 50,000.00 | |

3.3 AMERICAN SYSTEM

With interest capitalized during the waiting period

A financial institution lends $ 50,000.00 through the American System

to be paid after 5 years. What will be the value of the payment to be realized

on the due date, knowing that the interest are annually capitalized at

the rate of 12% per annum?

|

|

|

|

|

|

-50,000.00

|

|

|

|

12.000000

|

|

|

|

0.00

|

|

|

|

5.00

|

|

|

|

0.00

|

|

|

|

0.00

|

|

|

|

TO SOLVE

|

88,117.08

|

Answer: The value of the payment is $ 88,117.08.

| EVOLUTION SPREAD SHEET | ||||

| N | PAYMENT | INTEREST | PRINCIPAL | BALANCE |

| 0 | 50.000,00 | |||

| 1 | 0.00 | 6,000.00 | -6,000.00 | 56,000.00 |

| 2 | 0.00 | 6,720.00 | -6,720.00 | 62,720.00 |

| 3 | 0.00 | 7,526.40 | -7,526.40 | 70,246.40 |

| 4 | 0.00 | 8,429.57 | -8,429.57 | 78,675.97 |

| 5 | 88,117.08 | 9,441.12 | 78,675.96 | 0.00 |

| TOTAL | 88,117.08 | 38,117.08 | 50,000.00 | |

3.4 AMERICAN SYSTEM

With interest capitalized during the waiting period

Formation of the "Sinking Fund"

In the previous example, the debtor constitutes an amortization fund

at a financial institution that pays 10% per annum in order to avoid a

big outlay on the payment date. What is the value of the annual deposits?

|

|

|

|

|

|

0.00

|

|

|

|

10.000000

|

|

|

|

0.00

|

|

|

|

5.00

|

|

|

|

TO SOLVE

|

14,433.36

|

|

|

0.00

|

|

|

|

-88,117.08

|

|

Answer: The value of the annual deposits is $ 14,433.36.

| EVOLUTION SPREAD SHEET | ||||

| N | DEPOSIT | INTEREST | CAPITALIZATION | BALANCE |

| 1 | 14,433.36 | 0.00 | 14,433.36 | 14,433.36 |

| 2 | 14,433.36 | 1,443.34 | 15,876.69 | 30,310.05 |

| 3 | 14,433.36 | 3,031.00 | 17,464.36 | 47,774.41 |

| 4 | 14,433.36 | 4,777.44 | 19,210.80 | 66,985.20 |

| 5 | 14,433.36 | 6,698.52 | 21,131.88 | 88,117.08 |

| TOTAL | 72,166.78 | 15,950.30 | 88,117.08 | |

4.1 CANADIAN MORTGAGE

Postponed mode

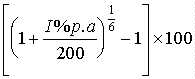

What is the necessary monthly payment to amortize a Canadian Mortgage of $ 10,000.00, with a term of 12 months, at an interest rate of 12%?

Note: as a preliminary procedure, the monthly interest rate must

be calculated through the formula:

( ( 1

+ I% p'a / 200 ) ^ ( 1 / 6 ) - 1 ) x 100

|

|

|

|

|

|

-10,000.00

|

|

|

|

0.975879

|

|

|

|

0.00

|

|

|

|

12.00

|

|

|

|

TO SOLVE

|

887.13

|

|

|

0.00

|

|

|

|

0.00

|

|

Answer: The necessary monthly payment is $ 887.13.

| EVOLUTION SPREAD SHEET | ||||

| N | PAYMENT | INTEREST | PRINCIPAL | BALANCE |

| 0 | 10,000.00 | |||

| 1 | 887.13 | 97.59 | 789.55 | 9,210.45 |

| 2 | 887.13 | 89.88 | 797.25 | 8,413.20 |

| 3 | 887.13 | 82.10 | 805.03 | 7,608.17 |

| 4 | 887.13 | 74.25 | 812.89 | 6,795.28 |

| 5 | 887.13 | 66.31 | 820.82 | 5,974.46 |

| 6 | 887.13 | 58.30 | 828.83 | 5,145.63 |

| 7 | 887.13 | 50.22 | 836.92 | 4,308.71 |

| 8 | 887.13 | 42.05 | 845.09 | 3,463.63 |

| 9 | 887.13 | 33.80 | 853.33 | 2,610.29 |

| 10 | 887.13 | 25.47 | 861.66 | 1,748.63 |

| 11 | 887.13 | 17.06 | 870.07 | 878.56 |

| 12 | 887.13 | 8.57 | 878.56 | 0.00 |

| TOTAL | 10,645.61 | 645.61 | 10,000.00 | |

5.1 GERMAN SYSTEM

What is the value of the installment of a $ 10,000.00 loan, for 6 years, at the rate of 12% per annum, through the German System?

Note: In the German System the interest are calculated and exacted

in advance. The first payment, which is exacted at the business transaction,

corresponds to a period of anticipated interest; the other installments

are used for amortization and interest, which are always anticipated.

|

|

|

|

|

|

-10,000.00

|

|

|

|

-12.000000

|

|

|

|

0.00

|

|

|

|

-6.00

|

|

|

|

TO SOLVE

|

-2,240.50

|

|

|

0.00

|

|

|

|

0.00

|

|

Answer: The value of the installment is $ 2,240.50

| EVOLUTION SPREAD SHEET | ||||

| N | PAYMENT | INTEREST | PRINCIPAL | BALANCE |

| 0 | 10,000.00 | |||

| 0 | 1,200.00 | 1,200.00 | 0.00 | 10,000.00 |

| 1 | 2,240.50 | 1,058.11 | 1,182.38 | 8,817.62 |

| 2 | 2,240.50 | 896.88 | 1,343.61 | 7,474.00 |

| 3 | 2,240.50 | 713.66 | 1,526.83 | 5,947.17 |

| 4 | 2,240.50 | 505.46 | 1,735.04 | 4,212.13 |

| 5 | 2,240.50 | 268.86 | 1,971.64 | 2,240.50 |

| 6 | 2,240.50 | 0.00 | 2,240.50 | 0.00 |

| TOTAL | 14,642.97 | 4,642.97 | 10,000.00 | |

6.1 SERIE IN CRESCENT GRADIENT

1st PMT = G

Postponed mode

An automobile is being sold in 5 monthly payments without down payment.

The first payment is $ 1,000.00; the second, $ 2,000.00; the third, $ 3,000.00;

the fourth, $ 4,000.00, and the fifth is $ 5,000.00. What is its value

at sight, knowing that the interest rate exacted by the financial institution

is 10% per month?

|

|

|

|

|

|

TO SOLVE

|

-10,652.59

|

|

|

10.000000

|

|

|

|

0.00

|

|

|

|

5.00

|

|

|

|

1,000.00

|

|

|

|

1,000.00

|

|

|

|

0.00

|

|

Answer: The value of the automobile at sight is $ 10,652.59.

| EVOLUTION SPREAD SHEET | ||||

| N | PAYMENT | INTEREST | PRINCIPAL | BALANCE |

| 0 | 10,652.59 | |||

| 1 | 1,000.00 | 1,065.26 | -65.26 | 10,717.85 |

| 2 | 2,000.00 | 1,071.78 | 928.22 | 9,789.63 |

| 3 | 3,000.00 | 978.96 | 2,021.04 | 7,768.60 |

| 4 | 4,000.00 | 776.86 | 3,223.14 | 4,545.46 |

| 5 | 5,000.00 | 454.55 | 4,545.45 | 0.00 |

| TOTAL | 15,000.00 | 4,347.41 | 10,652.59 | |

6.2 SERIE IN CRESCENT GRADIENT

1st PMT = G

Anticipated mode

Presuming that the first payment, in the previous example, is being

made at the business transaction, what will be the value of the automobile

at sight?

|

|

|

|

|

|

TO SOLVE

|

-11,717.85

|

|

|

10.000000

|

|

|

|

-1.00

|

|

|

|

5.00

|

|

|

|

1,000.00

|

|

|

|

1,000.00

|

|

|

|

0.00

|

|

Answer: The value of the automobile at sight is $ 11,717.85.

| EVOLUTION SPREAD SHEET | ||||

| N | PAYMENT | INTEREST | PRINCIPAL | BALANCE |

| 0 | 11,717.85 | |||

| 0 | 1,000.00 | 0.00 | 1,000.00 | 10,717.85 |

| 1 | 2,000.00 | 1,071.79 | 928.22 | 9,789.64 |

| 2 | 3,000.00 | 978.96 | 2,021.04 | 7,768.60 |

| 3 | 4,000.00 | 776.86 | 3,223.14 | 4,545.46 |

| 4 | 5,000.00 | 454.55 | 4,545.45 | 0.00 |

| TOTAL | 15,000.00 | 3,282.15 | 11,717.85 | |

6.3 SERIE IN CRESCENT GRADIENT

1st PMT = G

Deferred mode

In the previous example, what will be the value of the automobile at

sight if the first payment is made three months after the business transaction?

|

|

|

|

|

|

TO SOLVE

|

-8,803.79

|

|

|

10.000000

|

|

|

|

2.00

|

|

|

|

5.00

|

|

|

|

1,000.00

|

|

|

|

1,000.00

|

|

|

|

0.00

|

|

Answer: The value of the automobile at sight will be $ 8,803.79.

| EVOLUTION SPREAD SHEET | ||||

| N | PAYMENT | INTEREST | PRINCIPAL | BALANCE |

| 0 | 8,803.79 | |||

| 1 | 0.00 | 880.38 | -880.38 | 9,684.17 |

| 2 | 0.00 | 968.42 | -968.42 | 10,652.59 |

| 3 | 1,000.00 | 1,065.26 | -65.26 | 10,717.84 |

| 4 | 2,000.00 | 1,071.78 | 928.22 | 9,789.63 |

| 5 | 3,000.00 | 978.96 | 2,021.04 | 7,768.59 |

| 6 | 4,000.00 | 776.86 | 3,223.14 | 4,545.45 |

| 7 | 5,000.00 | 454.55 | 4,545.45 | 0.00 |

| TOTAL | 15,000.00 | 6,196.21 | 8,803.79 | |

6.4 SERIE IN CRESCENT GRADIENT

1st PMT # G

Postponed mode

A $ 10,000.00 loan will be settle at the rate of 10% per month. The

first installment - in value of $ 2,000.00 - expires one month after the

business transaction. What is the growth ratio so that it will be

possible to amortize the loan in 4 months?

|

|

|

|

|

|

-10,000.00

|

|

|

|

10.000000

|

|

|

|

0.00

|

|

|

|

4.00

|

|

|

|

2,000.00

|

|

|

|

TO SOLVE

|

836.04

|

|

|

0.00

|

|

Answer: The growth ratio is $ 836.04.

| EVOLUTION SPREAD SHEET | ||||

| N | PAYMENT | INTEREST | PRINCIPAL | BALANCE |

| 0 | 10,000.00 | |||

| 1 | 2,000.00 | 1,000.00 | 1,000.00 | 9,000.00 |

| 2 | 2,836.04 | 900.00 | 1,936.04 | 7,063.96 |

| 3 | 3,672.07 | 706.40 | 2,965.68 | 4,098.28 |

| 4 | 4,508.11 | 409.83 | 4,098.28 | 0.00 |

| TOTAL | 13,016.22 | 3,016.22 | 10,000.00 | |

7.1 CAPITALIZATION OF SERIES

IN CRESCENT

GRADIENT

1st PMT = G

Determine the amount acquired making 5 monthly deposits, knowing that

the first one is $ 1,000.00; the second, $ 2,000.00; the third, $ 3,000.00;

the fourth, $ 4,000.00, and the fifth one, $ 5,000.00. The interest rate

credited to the investor is 10% per month.

|

|

|

|

|

|

0.00

|

|

|

|

10.000000

|

|

|

|

0.00

|

|

|

|

5.00

|

|

|

|

1,000.00

|

|

|

|

1,000.00

|

|

|

|

TO SOLVE

|

-17,156.10

|

Answer: The amount acquired is $ 17,156.10.

| EVOLUTION SPREAD SHEET | ||||

| N | DEPOSIT | INTEREST | CAPITALIZATION | BALANCE |

| 1 | 1,000.00 | 0.00 | 1,000.00 | 1,000.00 |

| 2 | 2,000.00 | 100.00 | 2,100.00 | 3,100.00 |

| 3 | 3,000.00 | 310.00 | 3,310.00 | 6,410.00 |

| 4 | 4,000.00 | 641.00 | 4,641.00 | 11,051.00 |

| 5 | 5,000.00 | 1,105.10 | 6,105.10 | 17,156.10 |

| TOTAL | 15,000.00 | 2,156.10 | 17,156.10 | |

7.2 CAPITALIZATION OF SERIES

IN CRESCENT

GRADIENT

1st PMT # G

Intending to acquire an amount of $ 20,000.00, a person will make five

monthly deposits at a financial institution that pays 10% of interest per

month. Being aware that the first deposit will be $ 2,000.00, what is the

growth ratio that will allow the person to achieve the desired amount in

the foreseen term?

|

|

|

|

|

|

0.00

|

|

|

|

10.000000

|

|

|

|

0.00

|

|

|

|

5.00

|

|

|

|

2,000.00

|

|

|

|

TO SOLVE

|

704.90

|

|

|

-20,000.00

|

|

Answer: The growth ratio that will allow the person to achieve the desired amount in the foreseen term is $ 704.90.

| EVOLUTION SPREAD SHEET | ||||

| N | DEPOSIT | INTEREST | CAPITALIZATION | BALANCE |

| 1 | 2,000.00 | 0.00 | 2,000.00 | 2,000.00 |

| 2 | 2,704.90 | 200.00 | 2,904.90 | 4,904.90 |

| 3 | 3,409.79 | 490.49 | 3,900.28 | 8,805.18 |

| 4 | 4,114.69 | 880.52 | 4,995.20 | 13,800.38 |

| 5 | 4,819.58 | 1,380.04 | 6,199.62 | 20,000.00 |

| TOTAL | 17,048.95 | 2,951.05 | 20,000.00 | |

8.1 COMPOUND SYSTEM OF AMORTIZATION

WITH

REAL CRESCENT INSTALLMENTS

Postponed mode

A $ 30,000.00 loan was made by Compound System of Amortization with Real Crescent Installments in 36 months, at the interest rate of 2% per month. What is the value of the initial installment and the growth ratio to be reflected from the 25th installment on, knowing that the reducer is 15%?

1st STAGE: PMT calculation - French System of Amortization

|

|

|

|

|

|

-30,000.00

|

|

|

|

2.000000

|

|

|

|

0.00

|

|

|

|

36.00

|

|

|

|

TO SOLVE

|

1,176.99

|

|

|

0.00

|

|

|

|

0.00

|

|

2nd STAGE: Calculation of the balance in the date of the 23rd

PMT with reducer

|

|

|

|

|

|

-30,000.00

|

|

|

|

2.000000

|

|

|

|

0.00

|

|

|

|

23.00

|

|

|

|

1,000.44

|

|

|

|

0.00

|

|

|

|

TO SOLVE

|

18,449.39

|

3rd STAGE: Calculation of the growth ratio

|

|

|

|

|

|

-18,449.39

|

|

|

|

2.000000

|

|

|

|

0.00

|

|

|

|

13.00

|

|

|

|

1,000.44

|

|

|

|

TO SOLVE

|

109.26

|

|

|

0.00

|

|

Answer: The value of the initial installment is $ 1,000.44, and the growth ratio to be reflected from the 25th installment on, is $ 109.26.

| EVOLUTION SPREAD SHEET | ||||

| N | PAYMENT | INTEREST | PRINCIPAL | BALANCE |

| 0 | 30,000.00 | |||

| 1 | 1,000.44 | 600.00 | 400.44 | 29,599.56 |

| 2 | 1,000.44 | 591.99 | 408.45 | 29,191.12 |

| 3 | 1,000.44 | 583.82 | 416.62 | 28,774.50 |

| 4 | 1,000.44 | 575.49 | 424.95 | 28,349.55 |

| 5 | 1,000.44 | 566.99 | 433.45 | 27,916.11 |

| 6 | 1,000.44 | 558.32 | 442.12 | 27,473.99 |

| 7 | 1,000.44 | 549.48 | 450.96 | 27,023.03 |

| 8 | 1,000.44 | 540.46 | 459.98 | 26,563.06 |

| 9 | 1,000.44 | 531.26 | 469.18 | 26,093.88 |

| 10 | 1,000.44 | 521.88 | 478.56 | 25,615.32 |

| 11 | 1,000.44 | 512.31 | 488.13 | 25,127.19 |

| 12 | 1,000.44 | 502.54 | 497.89 | 24,629.29 |

| 13 | 1,000.44 | 492.59 | 507.85 | 24,121.44 |

| 14 | 1,000.44 | 482.43 | 518.01 | 23,603.43 |

| 15 | 1,000.44 | 472.07 | 528.37 | 23,075.06 |

| 16 | 1,000.44 | 461.50 | 538.94 | 22,536.13 |

| 17 | 1,000.44 | 450.72 | 549.72 | 21,986.41 |

| 18 | 1,000.44 | 439.73 | 560.71 | 21,425.70 |

| 19 | 1,000.44 | 428.51 | 571.92 | 20,853.78 |

| 20 | 1,000.44 | 417.08 | 583.36 | 20,270.42 |

| 21 | 1,000.44 | 405.41 | 595.03 | 19,675.39 |

| 22 | 1,000.44 | 393.51 | 606.93 | 19,068.46 |

| 23 | 1,000.44 | 381.37 | 619.07 | 18,449.39 |

| 24 | 1,000.44 | 368.99 | 631.45 | 17,817.94 |

| 25 | 1,109.70 | 356.36 | 753.34 | 17,064.60 |

| 26 | 1,218.95 | 341.29 | 877.66 | 16,186.94 |

| 27 | 1,328.21 | 323.74 | 1,004.47 | 15,182.47 |

| 28 | 1,437.47 | 303.65 | 1,133.82 | 14,048.64 |

| 29 | 1,546.73 | 280.97 | 1,265.76 | 12,782.89 |

| 30 | 1,655.99 | 255.66 | 1,400.33 | 11,382.56 |

| 31 | 1,765.24 | 227.65 | 1,537.59 | 9,844.97 |

| 32 | 1,874.50 | 196.90 | 1,677.60 | 8,167.36 |

| 33 | 1,983.76 | 163.35 | 1,820.41 | 6,346.95 |

| 34 | 2,093.02 | 126.94 | 1,966.08 | 4,380.87 |

| 35 | 2,202.28 | 87.62 | 2,114.66 | 2,266.21 |

| 36 | 2,311.54 | 45.32 | 2,266.21 | 0.00 |

| TOTAL | 44,537.89 | 14,537.89 | 30,000.00 | |

9.1 SERIE IN DECREASING GRADIENT

Final PMT = G

Postponed mode

Determine the value of an automobile, at sight, which will be paid in six decreasing, postponed monthly installments, knowing that the last payment - which is $ 1,000.00 - is equal to the monthly decreasing ratio. The hired interest rate is 5% per month.

Note: The value of the initial payment must be calculated as a

preliminary procedure, and it corresponds to ( G x N ).

|

|

|

|

|

|

TO SOLVE

|

-18,486.16

|

|

|

5.000000

|

|

|

|

0.00

|

|

|

|

6.00

|

|

|

|

6,000.00

|

|

|

|

-1,000.00

|

|

|

|

0.00

|

|

Answer: The sight value is $ 18,486.16.

| EVOLUTION SPREAD SHEET | ||||

| N | PAYMENT | INTEREST | PRINCIPAL | BALANCE |

| 0 | 18,486.16 | |||

| 1 | 6,000.00 | 924.31 | 5,075.69 | 13,410.47 |

| 2 | 5,000.00 | 670.52 | 4,329.48 | 9,080.99 |

| 3 | 4,000.00 | 454.05 | 3,545.95 | 5,535.04 |

| 4 | 3,000.00 | 276.75 | 2,723.25 | 2,811.79 |

| 5 | 2,000.00 | 140.59 | 1,859.41 | 952.38 |

| 6 | 1,000.00 | 47.62 | 952.38 | 0.00 |

| TOTAL | 21,000.00 | 2,513.84 | 18,486.16 | |

9.2 SERIE IN DECREASING GRADIENT

Final PMT = G

Anticipated mode

In the previous example, what would be the sight value of the automobile

if the first payment was made at the business transaction, in anticipated

form?

|

|

|

|

|

|

TO SOLVE

|

-19,410.47

|

|

|

5.000000

|

|

|

|

-1.00

|

|

|

|

6.00

|

|

|

|

6,000.00

|

|

|

|

-1,000.00

|

|

|

|

0.00

|

|

Answer: The automobile sight value would be $ 19,410.47.

| EVOLUTION SPREAD SHEET | ||||

| N | PAYMENT | INTEREST | PRINCIPAL | BALANCE |

| 0 | 19,410.47 | |||

| 0 | 6,000.00 | 0.00 | 6,000.00 | 13,410.47 |

| 1 | 5,000.00 | 670.52 | 4,329.48 | 9,080.99 |

| 2 | 4,000.00 | 454.05 | 3,545.95 | 5,535.04 |

| 3 | 3,000.00 | 276.75 | 2,723.25 | 2,811.80 |

| 4 | 2,000.00 | 140.59 | 1,859.41 | 952.39 |

| 5 | 1,000.00 | 47.62 | 952.38 | 0.00 |

| TOTAL | 21,000.00 | 1,589.53 | 19,410.47 | |

9.3 SERIE IN DECREASING GRADIENT

Final PMT = G

Deferred mode

In the previous example, what would be the sight value of the automobile

if the first payment was made three months after the business transaction?

|

|

|

|

|

|

TO SOLVE

|

-16,767.49

|

|

|

5.000000

|

|

|

|

2.00

|

|

|

|

6.00

|

|

|

|

6,000.00

|

|

|

|

-1,000.00

|

|

|

|

0.00

|

|

Answer: The automobile sight value would be $ 16,767.49.

| EVOLUTION SPREAD SHEET | ||||

| N | PAYMENT | INTEREST | PRINCIPAL | BALANCE |

| 0 | 16,767.49 | |||

| 1 | 0.00 | 838.37 | -838.37 | 17,605.86 |

| 2 | 0.00 | 880.29 | -880.29 | 18,486.16 |

| 3 | 6,000.00 | 924.31 | 5,075.69 | 13,410.47 |

| 4 | 5,000.00 | 670.52 | 4,329.48 | 9,080.99 |

| 5 | 4,000.00 | 454.05 | 3,545.95 | 5,535.04 |

| 6 | 3,000.00 | 276.75 | 2,723.25 | 2,811.79 |

| 7 | 2,000.00 | 140.59 | 1,859.41 | 952.38 |

| 8 | 1,000.00 | 47.62 | 952.38 | 0.00 |

| TOTAL | 21,000.00 | 4,232.51 | 16,767.49 | |

9.4 SERIE IN DECREASING GRADIENT

Final PMT # G

Postponed mode

Determine the value at sight of a property, to be paid in six monthly postponed installments, knowing that the value of the last payment is $ 5,000.00 and that the installments decrease at the ratio of $ 1,000.00. The hired interest rate is 5% per month.

Note: Calculate, first, the value of PMT as being the last PMT

+ G x ( n - 1 ).

|

|

|

|

|

|

TO SOLVE

|

-38,788.93

|

|

|

5.000000

|

|

|

|

0.00

|

|

|

|

6.00

|

|

|

|

10,000.00

|

|

|

|

-1,000.00

|

|

|

|

0.00

|

|

Answer: The sight value of the property is $ 38,788.93.

| EVOLUTION SPREAD SHEET | ||||

| N | PAYMENT | INTEREST | PRINCIPAL | BALANCE |

| 0 | 38,788.93 | |||

| 1 | 10,000.00 | 1,939.45 | 8,060.55 | 30,728.38 |

| 2 | 9,000.00 | 1,536.42 | 7,463.58 | 23,264.80 |

| 3 | 8,000.00 | 1,163.24 | 6,836.76 | 16,428.04 |

| 4 | 7,000.00 | 821.40 | 6,178.60 | 10,249.44 |

| 5 | 6,000.00 | 512.47 | 5,487.53 | 4,761.91 |

| 6 | 5,000.00 | 238.10 | 4,761.90 | 0.00 |

| TOTAL | 45,000.00 | 6,211.07 | 38,788.93 | |

10.1 CAPITALIZATION OF SERIE IN DECREASING

GRADIENT

Final PMT = G

An investor made six monthly deposits. The last one, in value of $ 1,000.00, was equal to the monthly decreasing ratio. What was the acquired amount, knowing that the hired interest rate was 5% per month?

Note: The value of the initial deposit must be calculated as a

preliminary procedure, and it corresponds to ( G x N ).

|

|

|

|

|

|

0.00

|

|

|

|

5.000000

|

|

|

|

0.00

|

|

|

|

6.00

|

|

|

|

6,000.00

|

|

|

|

-1,000.00

|

|

|

|

TO SOLVE

|

-24,773.22

|

Answer: The acquired amount was $ 24,773.22.

| EVOLUTION SPREAD SHEET | ||||

| N | DEPOSIT | INTEREST | CAPITALIZATION | BALANCE |

| 1 | 6,000.00 | 0.00 | 6,000.00 | 6,000.00 |

| 2 | 5,000.00 | 300.00 | 5,300.00 | 11,300.00 |

| 3 | 4,000.00 | 565.00 | 4,565.00 | 15,865.00 |

| 4 | 3,000.00 | 793.25 | 3,793.25 | 19,658.25 |

| 5 | 2,000.00 | 982.91 | 2,982.91 | 22,641.16 |

| 6 | 1,000.00 | 1,132.06 | 2,132.06 | 24,773.22 |

| TOTAL | 21,000.00 | 3,773.22 | 24,773.22 | |

10.2 CAPITALIZATION OF SERIE IN DECREASING

GRADIENT

Final PMT # G

A person intends to obtain $ 20,000.00 making 6 monthly deposits at

a financial institution that pays 5% per month. Knowing that the first

deposit will be $ 5,000.00, what should be the value of the gradient so

that the desired amount is reached in the foreseen term?

|

|

|

|

|

|

0.00

|

|

|

|

5.000000

|

|

|

|

0.00

|

|

|

|

6.00

|

|

|

|

5,000.00

|

|

|

|

TO SOLVE

|

-873.51

|

|

|

-20,000.00

|

|

Answer: The gradient value should be $ 873.51, decreasing.

| EVOLUTION SPREAD SHEET | ||||

| N | DEPOSIT | INTEREST | CAPITALIZATION | BALANCE |

| 1 | 5,000.00 | 0.00 | 5,000.00 | 5,000.00 |

| 2 | 4,126.49 | 250.00 | 4,376.49 | 9,376.49 |

| 3 | 3,252.98 | 468.82 | 3,721.81 | 13,098.30 |

| 4 | 2,379.47 | 654.91 | 3,034.39 | 16,132.68 |

| 5 | 1,505.96 | 806.63 | 2,312.60 | 18,445.28 |

| 6 | 632.45 | 922.26 | 1,554.72 | 20,000.00 |

| TOTAL | 16,897.36 | 3,102.64 | 20,000.00 | |

11.1 CONSTANT AMORTIZATION SYSTEM

Postponed mode

A $ 10,000.00 loan, hired at the interest rate of 10% per month, will be paid in 4 monthly installments through the Constant Amortization System. The first installment expires one month after the business transaction. What will be the value of the initial installment?

Note: The value of the monthly decreasing ratio, or negative ratio,

which corresponds to ( PV / N ) x ( I% / 100 ), must be calculated as a

preliminary procedure.

|

|

|

|

|

|

-10,000.00

|

|

|

|

10.000000

|

|

|

|

0.00

|

|

|

|

4.00

|

|

|

|

TO SOLVE

|

3,500.00

|

|

|

-250.00

|

|

|

|

0.00

|

|

Answer: The value of the initial installment will be $ 3,500.00.

| EVOLUTION SPREAD SHEET | ||||

| N | PAYMENT | INTEREST | PRINCIPAL | BALANCE |

| 0 | 10,000.00 | |||

| 1 | 3,500.00 | 1,000.00 | 2,500.00 | 7,500.00 |

| 2 | 3,250.00 | 750.00 | 2,500.00 | 5,000.00 |

| 3 | 3,000.00 | 500.00 | 2,500.00 | 2,500.00 |

| 4 | 2,750.00 | 250.00 | 2,500.00 | 0.00 |

| TOTAL | 12,500.00 | 2,500.00 | 10,000.00 | |

12.1 COMPOUND SYSTEM OF AMORTIZATION

Postponed mode

A $ 10,000.00 loan, hired at the rate of 10% per month, will be paid in 4 monthly installments through the Compound System of Amortization. The first installment expires one month after the business transaction. What will be the value of the initial installment?

Note: The value of the monthly decreasing ratio, or negative ratio,

which corresponds to ( PV / N ) x ( I% / 200 ), must be calculated as a

preliminary procedure.

|

|

|

|

|

|

-10,000.00

|

|

|

|

10.000000

|

|

|

|

0.00

|

|

|

|

4.00

|

|

|

|

TO SOLVE

|

3,327.35

|

|

|

-125.00

|

|

|

|

0.00

|

|

Answer: The value of the initial installment will be $ 3,327.35.

| EVOLUTION SPREAD SHEET | ||||

| N | PAYMENT | INTEREST | PRINCIPAL | BALANCE |

| 0 | 10,000.00 | |||

| 1 | 3,327.35 | 1,000.00 | 2,327.35 | 7,672.65 |

| 2 | 3,202.35 | 767.26 | 2,435.09 | 5,237.56 |

| 3 | 3,077.35 | 523.76 | 2,553.60 | 2,683.96 |

| 4 | 2,952.35 | 268.40 | 2,683.96 | 0.00 |

| TOTAL | 12,559.42 | 2,559.42 | 10,000.00 | |

I would like to inform you that the examples enclosed in the work are only basic problems of each type of amortization system or capitalization plan, however, the method allows a multiplicity of combinations of calculations which are always executed with the single generic formula, object of the "Liebl Method".

Among the possible calculations are:

- loans and financing in the anticipated, postponed and deferred modes,

with float, flat, and combined flat and float;

- capitalization plans;

- settlement of debits to anticipated payment;

- extraordinary amortization for reduction of the installment

value;

- extraordinary amortization for reduction of the financing term;

- extraordinary amortization for reduction of the installment value

and financing term, combined;

- incorporation of the overdue payments with the raise of the installment

value;

- incorporation of the overdue payments with the extension of the financing

term;

- incorporation of the overdue payments with the raise of the installment

value and extension of the financing term, combined;

- renegotiation of the loan with extension of the term;

- renegotiation of the loan with reduction of the term;

- renogotiation of the loan with reduction of the interest rate;

- renegotiation of the loan with the raise of the interest rate;

- renegotiation of the loan with alteration of amortization system;

- renegotiation of the loan with alteration of amortization system,

term and/or interest rate combined.

With the aim of continuing the development of the researches to implement these innovations, I would like to count on the support and sponsorship of a renowned educational institution or companies that have some interest on it. I am at your disposal to present my thesis to the scientific community and experts in the subject.

I am at your disposal to any additional explanation.

Respectfully yours,

Jonas Liebl

E-mail: jonasliebl@netpar.com.br